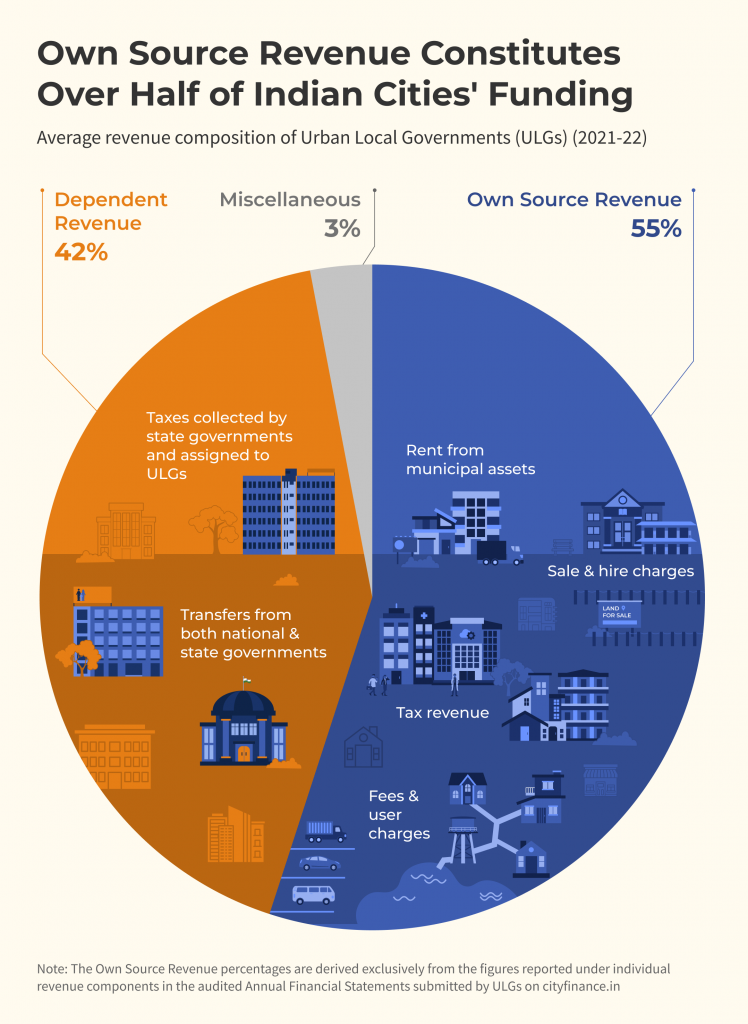

A city’s fiscal autonomy is only as strong as the revenue it generates on its own and, as our last blog post showed, that autonomy is far from evenly distributed. But what exactly makes up that revenue?

In our previous blog post, we explored how Own Source Revenue (OSR) is generated across cities of different sizes and states. OSR is not a single revenue stream; it is a combination of different revenue components that Urban Local Governments (ULGs) generate through their taxation powers, service delivery functions and assets. Each of these components contributes differently, shaping the overall structure of municipal own revenue.

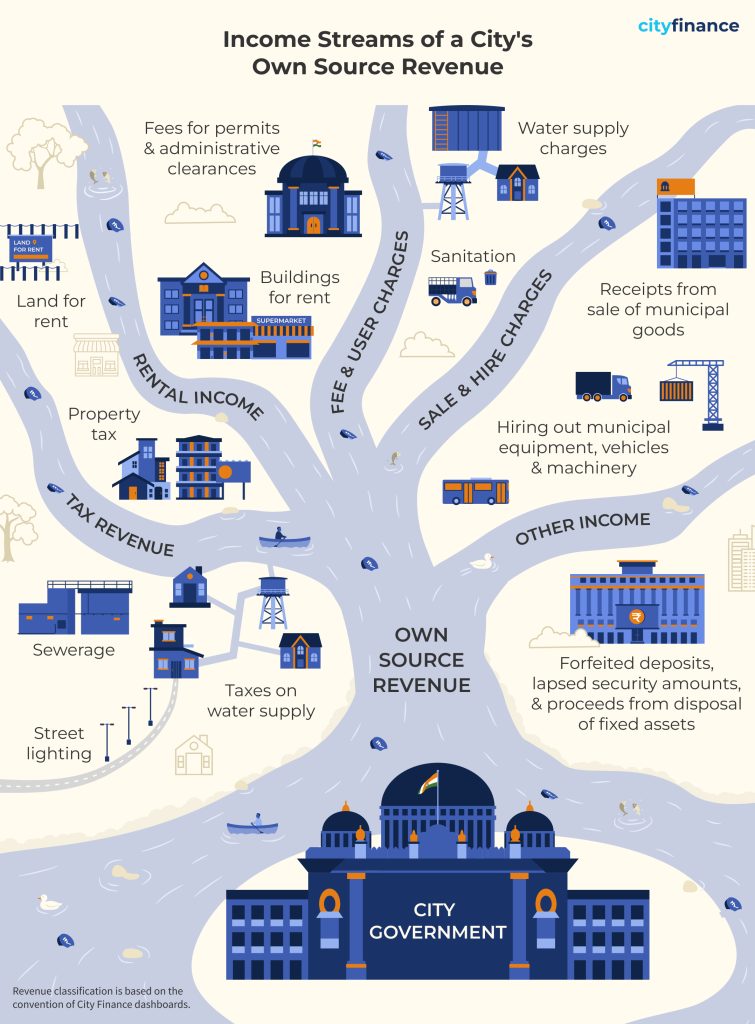

At its core, OSR comprises two broad categories: tax and non-tax revenue. Tax revenue is dominated by property tax, alongside levies on water supply, sewerage, conservancy, street lighting, education, and other municipal services.

Non-tax revenue is more diverse and includes fees and user charges for services such as water supply, sanitation, and solid waste management, as well as payments for licenses, permits, and regulatory approvals. Other important components include sale and hire charges, generated from the sale of municipal goods and the hiring of municipal equipment or vehicles, and rental income from leasing municipal assets such as shops, markets, community halls, and land.

OSR also includes a residual category termed ‘other income,’ comprising receipts such as forfeited deposits, employee recoveries, disposal of assets, and various accounting adjustments. Unlike taxes and user charges, these receipts are often irregular and unpredictable.

The average composition of Own Source Revenue of Indian ULGs across FY 2019–20 to FY 2021–22 highlights the continued dominance of tax revenue, which accounts for half of total OSR. Fees and user charges constitute the second-largest component at 32 per cent, underscoring the importance of service-linked non-tax revenues in municipal finances. Other income contributes 14 per cent, while rental income (3 per cent) and sale and hire charges (1 per cent) together form a relatively small share. Overall, the revenue mix suggests that municipal finances remain anchored in taxation, with non-tax sources, particularly fees and user charges, playing an important, complementary role in strengthening local revenue generation.

From Small Towns to Megacities: A Telling Revenue Picture

FY 2021–22 data shows that tax revenue remains the primary source of OSR for most Indian cities. The notable exception is 4-million-plus cities (4M+ cities), where fees and user charges account for the largest share (47 per cent). 4M+ cities and cities with population less than 100K show a relatively higher share of ’other income’. In contrast, sale and hire charges remain marginal across all city categories.

ULGs of a majority of Indian states exhibit limited diversification in their OSR structures, with heavy reliance on tax revenue and fees and user charges. In 12 out of 24 states analysed, these two sources together account for more than 75 per cent of total OSR. Rental income remains a minor contributor in most states, averaging around 15 per cent across the sample. Sale and hire charges are negligible almost universally, rarely exceeding 10 per cent.

Key Takeaways

The composition of a city’s Own Source Revenue tells a story not just of how much OSR it raises, but of how it raises it and how sustainably it can do so. Across Indian states, the picture is one of limited diversification, a heavy reliance on tax revenue and fees and user charges, with rental income and other receipts remaining largely untapped.

Improving Own Source Revenue is not just about diversifying revenue streams. It demands strengthening collection efficiency within existing sources, rationalising fee structures, and reducing dependence on a narrow own revenue base. Achieving this, however, demands skills and capacities that many ULGs, particularly smaller ones, currently lack. Hence, strengthening local capacity is an equally important priority. As cities face growing expenditure pressures, building a more resilient and self-sufficient municipal finance system is not just a fiscal imperative, it is foundational to delivering better urban services and stronger local governance.

Stay tuned for a closer look at the key components of Own Source Revenue of cities.

Note: All data is sourced from the Annual Financial Statements submitted by the ULGs on the CityFinance platform. To ensure comprehensive representation and account for variations in data coverage and quality across cities, the figures presented are based on extrapolated financial data covering all 4,824 cities. Among these, 2,541 cities (approximately 60%) possess 3 years of contiguous data (2019–20 to 2021–22) in Cityfinance platform. Data from these cities have been systematically extrapolated using the ’per capita scaling methodology’ to reflect the financial performance of the complete set of 4,824 cities. Learn more about the extrapolation methodology here.